Telefónica is at a point where it’s no longer inherently expensive, but there aren’t any near-term catalysts that could propel the stock higher, explains José Lizán, manager of retro magnum sicavs at Quadriga. If there is anything that could impact the price it is from a negative perspective as it could be the sale of Vodafone Spain to venture capital that could shake up the market.

There’s a market rumor that Vodafone could leave Spain (one of the group’s worst divisions) and give way to one of those venture capital funds with big financial power. This would be negative for Telefónica, as further integration movement in the industry with smaller mobile operators would be on the horizon, allowing for a renewed rationalization of the market, which would create more competitive pressures in the industry.

From a business perspective, Telefónica is in a sensible moment, growing at moderate rates in both Ebitda and revenue. It has cost inflation but has been able to raise prices to adequately weather those increases. In any case, they fail to continue the deleveraging process that has been positively pursued in the past because it is more complicated in a scenario of rising interest rates.

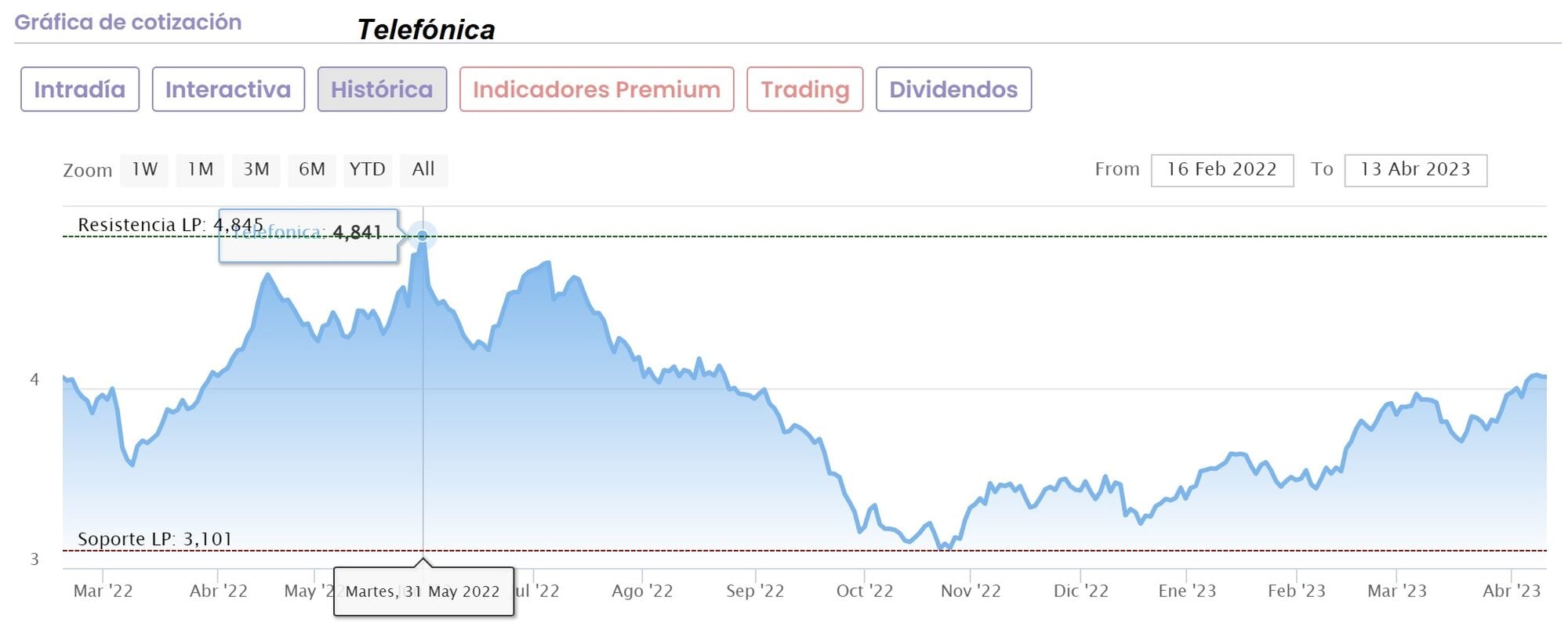

The expert has been expecting a large sideways movement for Telefónica for quite some time, which will be very difficult to exceed 5 euros, and if below 4 euros would be a buy, “I think that if there are no big catalysts, it will move in this sector “. Other names in this sector are doing well and acting as defensive stocks, which also supports Telefónica.

In May of last year, it was able to approach the EUR 5 level, but not break through to the upside:

As explained Javier Alfayate, Managing Director of GPM Sociedad de Valoresthe telecom companies are doing quite well and there are other stocks that are doing better than Telefónica, like Deutsche Telekom or KPN.

For Telefónica, good because it has exceeded 4 euros, but its behavior is mediocre, it is in the 53rd percentile, in the middle part of the table in relation to the rest of the components in the same sector. The expert would not have it in their portfolio now and would choose a different name. But as long as you respect the 3.70 euros, if we already have it in the portfolio, you can keep it.

Analyst consensus collected by Reuters gives to give advice to Telefónica and a price target of €4.4, which represents an upside of around 8.6% from Friday’s price.